z31maniac wrote:

Swank Force One wrote:

nicksta43 wrote:

I'm looking at my cost of the plan. My employer, as far as I know , cover 0. What I got is what will come out of my check every two weeks.

If your employer is covering 0%, then they aren't really providing you with health insurance. I'm not sure if that's illegal or not, but it's certainly stupid and worthless.

You should definitely be looking at private/exchange.

And a new job, in my opinion. That's IF there isn't a miscommunication somewhere.

Yeah, that doesn't seem right. For instance I pay $88 every two weeks for dental/vision/health for my wife and I (HSA plan) and my employer pays about another $260 every two weeks for those as well.

But your also paying $6400 or whatever the current year max contribution to you HSA account is right.. Right..?

I had an HSA at my previous employer. I want back in. We pay ~$500/month now plus some copays (which come out of my HSA that still have ~10K in it but I can't contribute anymore). the HSA overall was nearly equivalent in annual spend but we always ended up with extra and the max out of pocket was lower and all insurance moneys where tax free.

Duke

PowerDork

8/21/13 10:13 a.m.

DILYSI Dave wrote:

I'm about 50% sure that in the next couple of years I'm going to just dump insurance and pay the fee. I've never been one to work the system, but in this case I feel like the system is working me. I did what I could to stop us from getting here, but now that we're here, berkeley it - time to get mine.

Understand - that's exactly what the government wants. They want this plan to be a stupendously expensive clusterberk for the average person, so that they can step back in and say "See, we told you that National Health Service was a better idea!"

To Nicksta, good luck, man. My wife's company currently provides almost-decent family insurance for an almost-decent cost. I'm dreading the news in about 6 weeks, when we need to enroll for next year.

No, I get that. I'm just tired of fighting the good fight. I'm just trying to stay enough ahead of the boulder that I can collect enough "retire in Costa Rica" money before it catches up.

z31maniac wrote:

poopshovel wrote:

I don't know how the hell you're gonna keep this one from getting political. The jump in rates is not a coincidence. Just be happy you get to keep your 40+ hrs a week...or, even better, you're on salary. Good luck.

Also: Obviously not a fan of Obamacare, but your "per person, PER MONTH" thing is way off. If a couple hundred bucks a year is going to "bankrupt" you, I'd definitely look into medicaid. You're obviously paying in. Get your money back.

He did mention 24% of their household income, not an insignificant chunk of change. For my wife and I, that would be quite a bit more (% wise ) than our house payment.

That's insane.

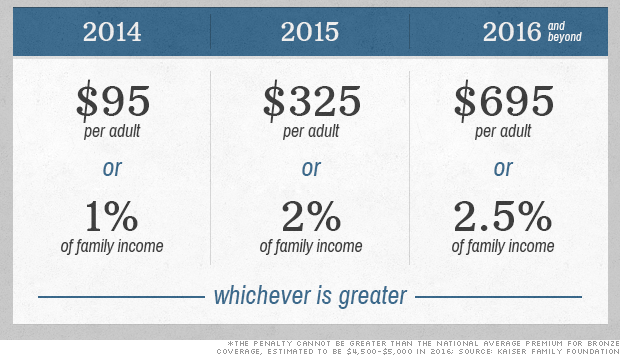

From CNN:

So next year, the penalty will either be $95 per adult, or 1% of the family's income, ASSUMING he rejects the company's plan and buys a (presumably WAAAAAAAAAY cheaper) private plan.

I'm not saying it's right, but it's way less than "$95 per person per month." Get a quote for a catastrophic plan with HSA. Shouldn't be anywhere near as grim as the company's rates.

Personally, I'd wait till October and sign up fo dem freeee buhnufits @ healthcare.gov.

DILYSI Dave wrote:

I'm about 50% sure that in the next couple of years I'm going to just dump insurance and pay the fee. I've never been one to work the system, but in this case I feel like the system is working me. I did what I could to stop us from getting here, but now that we're here, berkeley it - time to get mine.

As I understand the law you can't dump coverage and just pay the fee if your employer offers coverage. Been wrong before, will be wrong again.

In reply to poopshovel:

But the option to buy a private insurance is not on available anymore. Can not buy it.

nicksta43 wrote:

In reply to poopshovel:

But the option to buy a private insurance is not on available anymore. Can not buy it.

I believe you are incorrect here. Seriously, have you gone to the healthcare.gov website and filled out the survey? I did it for you, and it says you "may" still be eligible for coverage, even though your employer already provides it, under the exchange deal.

http://www.youtube.com/watch?v=W1ht8msGqwI

mtn

UltimaDork

8/21/13 10:50 a.m.

nicksta43 wrote:

In reply to poopshovel:

But the option to buy a private insurance is not on available anymore. Can not buy it.

Gov't won't let you, you cannot afford it, or it is not available?

Went to the agent who got us our private insurance previously. And another because we were a little skeptical . Both said we couldn't. I'm not in the insurance business, just know what I was told.

Edit; we could not because both of our employers offer health insurance. What I got from it is it's either through the exchange or employer, private health insurance will not exist come January 1st. But like I said I hope I'm wrong.

nocones wrote:

z31maniac wrote:

Swank Force One wrote:

nicksta43 wrote:

I'm looking at my cost of the plan. My employer, as far as I know , cover 0. What I got is what will come out of my check every two weeks.

If your employer is covering 0%, then they aren't really providing you with health insurance. I'm not sure if that's illegal or not, but it's certainly stupid and worthless.

You should definitely be looking at private/exchange.

And a new job, in my opinion. That's IF there isn't a miscommunication somewhere.

Yeah, that doesn't seem right. For instance I pay $88 every two weeks for dental/vision/health for my wife and I (HSA plan) and my employer pays about another $260 every two weeks for those as well.

But your also paying $6400 or whatever the current year max contribution to you HSA account is right.. Right..?

I had an HSA at my previous employer. I want back in. We pay ~$500/month now plus some copays (which come out of my HSA that still have ~10K in it but I can't contribute anymore). the HSA overall was nearly equivalent in annual spend but we always ended up with extra and the max out of pocket was lower and all insurance moneys where tax free.

Nope, I guess actually my employer contributes even more because they drop another $1200-1400 a year in my account along with what I do.

I'm just about up to my out of pocket limit on my HSA, at which point, I will lower my contribution and put more in my 401k. I'm not particularly worried because I could stop my after tax savings for a 4 months + a big contribution and be to the max, if something happened and I need to replenish it.

We are young with no kids, so once we have that, I'll throw $20 a check and let the company keep putting money in as well.

I know how much I have to pay out of pocket. $13200 more per year than I am now.

Fletch1

HalfDork

8/21/13 11:07 a.m.

In reply to poopshovel:

I just choked on my turkey sandwich as I was expecting a different video.

nicksta43 wrote:

I know how much I have to pay out of pocket. $13200 more per year than I am now.

You still seriously need to verify that number with HR, talking with someone who actually knows what they talk about.

I'm telling you you'd have to try VERY hard to even get an insurance policy for 2 adults and a kid that costs that much.

Verified and re verified. That's what will come out of my check with this plan. HR says they are working on something better hopefully have some news around October.

“if you like your current plan, you can keep it until you can't”

FTFY

yamaha

PowerDork

8/21/13 12:36 p.m.

I'm by myself, and I'm worried my if my company will continue to contribute as much as they do now.....its not a great plan, but its good enough for me. I think I am paying in around $20/mo as a smoker.....we don't have HSA's either.

chrispy

New Reader

8/21/13 12:53 p.m.

I work for a small company and noticed my HR person is here way longer than usual. I've been fortunate (spoiled) to have very affordable coverage for myself (100% employer paid) but I've seen the writing on the wall. My wife has also had excellent coverage and its been cheaper for her to cover herself and the kids than add them to my policy. She works for a big company so we'll see how this affects us too. Thanks for this post and good luck.

nderwater wrote:

I just took a look at my pay stubs - I'm paying about $650 a month ($7800/yr pretax) for medical/dental coverage for a family of four, and I'm bracing for that to go up significantly next year. I get angry every time I think about it, but what can you do?

Med care has to change. That's about all we can do. The profit taking is out of control.

One medical companies profits (cough McKeeson! cough) has been up 8% in the last 5 years. Net profit of $521 million. Revenue is $30 Billion. Link The CEO would make a lump sum payment of $159 million if he retired. CTW Investment group says McKesson is "the new poster-child of out-of-control CEO pay.". Link This affects how much you pay for insurance.

Maybe it's time we stop voting between the two false choices of D's and R's and started voting in our own interests instead of theirs?

Swank Force One wrote:

nicksta43 wrote:

I'm looking at my cost of the plan. My employer, as far as I know , cover 0. What I got is what will come out of my check every two weeks.

If your employer is covering 0%, then they aren't really providing you with health insurance. I'm not sure if that's illegal or not, but it's certainly stupid and worthless.

You should definitely be looking at private/exchange.

And a new job, in my opinion. That's IF there isn't a miscommunication somewhere.

Get'em Swank Force! You speak the truth!

I've not looked too deeply into things with the ACA- I've been on a 'high deductible w/ preventative care & HSA' plan for several years now where my employer pays the entirety of the premium and I just contribute to the savings account since they started offering it a few years back- but from what I have been able to find in researching it quickly it really sounds like something fishy is up with your company's insurance.

According to the Healthcare.gov site info on what happens if you have job-based coverage (https://www.healthcare.gov/what-if-i-have-job-based-health-insurance/), if your coverage is (as they define it) 'affordable' and meets the minimum requirements, you're not eligible for lower-cost premiums or out-of-pocket costs in the Marketplace. BUT- as was previously stated, the definition of 'affordable' for self-only coverage is no more than 9.5% of household income (https://www.healthcare.gov/glossary/affordable-coverage/). If you're paying over 50% of your income (potentially less than 50% of household though if you both work) than it sounds like the employer coverage doesn't meet that requirement. However, some of the employer requirements have been deferred... so it's hard to tell if you can do anything about it now.

There is also the requirement that any increase of more than 10% is supposed to be 'publicly justified' (https://www.healthcare.gov/how-does-the-health-care-law-protect-me/), so the 700% jump you're seeing sounds WAY out there.

Part of me wonders if there's not something more at work here, like an effort by the company or insurer trying to milk people for as much as they can before they're limited by the defered requirements or trying to drum up opposition to the ACA by blaming huge increases on its requirements. Despite (or perhaps BECAUSE of...) working for a huge corporation, I have a tendency to solidly distrust their actions & motives...

Well, E36 M3 man. That doesn't sound right, but I'm not an insurance agent, and I'd think they'd be chomping at the bit to sell you a policy if they could. I'd at least wait till October and see what happens after the E36 M3 hits the fan.

I'm having a hard time understanding why your company can't negotiate a cheaper policy. I'm assuming this is the uber ultra mega cadillac plan they're pricing out for you.

If everything is as you say it is, I'd ditch the insurance altogether and pay the penalty. Spend $60 cash for a doctor's visit when you get sick, and $4 for antibiotics. If someone gets cancer, buy the insurance then. They CAN'T deny you coverage anymore, right Nancy? Nancy?

http://www.youtube.com/watch?v=W1ht8msGqwI

Either way, I wouldn't stress about it too much. Something seems way the berkeley off.

SCARR

Reader

8/21/13 1:08 p.m.

so.... according to your posts you make about 30k a year, and pay about 158 dollars a month for insurance. that is still pretty good, if your employer is paying nothing, as the average cost of health insurance for the year for a person is 5k. and the new plan changes to $15,085 for 3 people? still sounds correct.

the problem is entirely that your employer does not give the benefit of paying part of your health insurance costs.

honestly, look for a new Job. you work for a rare company.

This whole transition is going to be hard for a lot of people. Part of what seems to be going on (this coming from conversations I've had with people) is that there is an increased benefit to some employers to hand off pretty much the full cost of healthcare on their employees. In the past they risked losing employees because they needed the healthcare, or they would get sick and not be covered and not able to work. Now everyone is in the same boat and not covering a significant part of their employees cost doesn't really hurt them.

The big part of this is that a lot of people are seeing the true cost of their healthcare for the first time and it's blowing their minds. Medical costs in the US and the insurance to cover them are crushingly expensive. My wife's grandfather just had a minor stroke. He's doing well but has been in the hospital for three weeks, had an helicopter ride from one hospital to another, had a pacemaker installed because somehow the stroke made his heart forget how to beat right, and is now battling a secondary pneumonia. He never paid enough into the system in his entire life to cover the last month. My dad just had a knee replaced. Couple that with the other knee that needs to be done, his neck surgery a decade ago, and being successfully treated for prostate cancer and you have a HUGE pile of money. $1k a month is a lot, but not in comparison to what he has received. My son stepped on a nail this last spring and got three days in the hospital on IV antibiotics for it. Freak thing, the nail infected the joint capsule in his big toe and losing part of his foot was a real possibility. $45k, and that was cheap because things went well and he didn't need surgery.

This is what medicine costs. This is what it has cost for the past decade. It's going to come out of taxes or our pay or something.

Duke

PowerDork

8/21/13 2:17 p.m.

Xceler8x wrote:

Med care has to change. That's about all we can do. The profit taking is out of control.

One medical companies profits (cough McKeeson! cough) has been up 8% in the last 5 years. Net profit of $521 million. Revenue is $30 Billion.

By my calculations, that's a profit margin of 17.36%. A good margin, indeed, but hardly usurious, evil, or "out of control". That also says nothing about ROI. How long have they had the money committed that is making that profit also affects the real value of that profit margin. If that's the end result of a 5-year investment, the actual return is considerably lower than if it was a 6-month windfall.

Duke wrote:

Xceler8x wrote:

Med care has to change. That's about all we can do. The profit taking is out of control.

One medical companies profits (cough McKeeson! cough) has been up 8% in the last 5 years. Net profit of $521 million. Revenue is $30 Billion.

By my calculations, that's a profit margin of 17.36%. A good margin, indeed, but hardly usurious, evil, or "out of control". That also says nothing about ROI. How long have they had the money committed that is making that profit also affects the real value of that profit margin. If that's the end result of a 5-year investment, the actual return is considerably lower than if it was a 6-month windfall.

Besides the outsized salary I agree with you. That, in and of itself, isn't horrible. In fact, making a profit is fine as long as it isn't at the expense of our nation's security, economic prosperity for the economy as a whole, or causing mass amounts of hardship on people. No amount of profit is ok if people or the U.S. suffers outrageously when it is taken. Pile that on top of everyone else taking their profit and you have a horrendous and burdensome cost that we as consumers are just starting to see and experience.

Another example. Hospital charges. Here are some great articles on the subject.

Hospital Costs Go Public: What Changes In Health Care?

Bitter Pill: Why Medical Bills Are Killing Us

New Report Shows Staggering Differences in the Cost of Medical

Treatments

It's not just the cost difference in hospitals sometimes just miles apart but the markup that they charge. A quote from the last article:

"Steven Brill, who wrote extensively about ballooning medical costs for Time Magazine, explained on the PBS NewsHour how hospitals often pad the costs in their chargemasters.

"They're typically five to 10 times what it costs the hospital to buy those items or provide those items," he said. "And insurance companies get big discounts off of the chargemaster, but the discounts that they get are still not enough to keep these hospitals from making very high profit margins and from all the non-doctor administrators at these hospitals from making exorbitant salaries."

This profit taking on top of McKeeson's profit taking, to support outsized salaries in part, are at least one cause of the current huge cost to us and the nation for health care. It can't continue no matter how you feel about what's an appropriate profit level. We just can't afford for profits to grow at these rates as indicated by what started this post.

It's really not about politics at this point. It's economics.

tuna55

PowerDork

8/21/13 3:00 p.m.

Xceler8x wrote:

It's really not about politics at this point. It's economics.

uhhhh - OK.

Health care costs are out of control. But everything you just said was all about politics and had basically nothing to do with economics.